Daring 12A Registration: Empower Your Cause with 80G Guide

Introduction

Starting a charitable trust or NGO is a noble step.

But to ensure tax benefits — both for the organization and its donors — proper registration under the Income-tax Act is essential.

Two key registrations every charitable organization must understand are:

Section 12A / 12AB Registration

Section 80G Registration

These registrations help NGOs claim income tax exemption and allow donors to claim tax deduction.

Let’s understand this in a simple and structured manner.

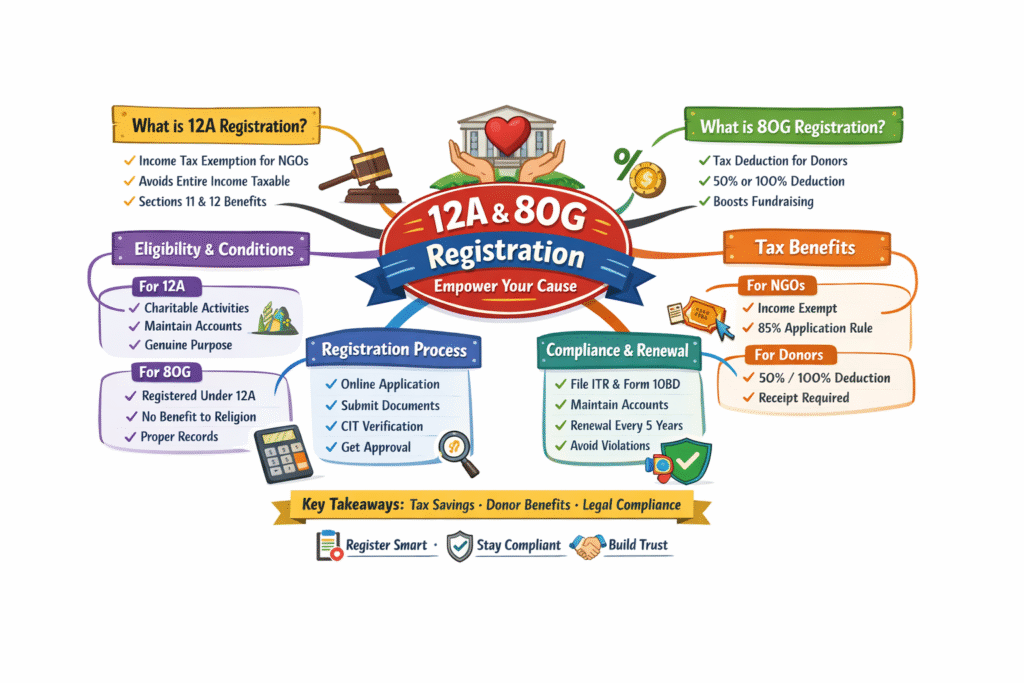

What is 12A Registration?

Section 12A (now governed through Section 12AB) of the Income-tax Act provides income tax exemption to trusts and institutions established for charitable or religious purposes.

Without 12A/12AB registration:

❌ Entire income of the trust becomes taxable

❌ No exemption under Sections 11 and 12 is available

With registration:

✔ Income applied for charitable purposes becomes exempt

✔ Accumulated income (subject to conditions) is allowed

✔ Trust is treated as a charitable institution under tax law

What is 80G Registration?

Section 80G allows donors to claim deduction on donations made to eligible charitable institutions.

If an NGO has 80G registration:

✔ Donors can claim deduction (50% or 100% depending on category)

✔ Helps attract funding

✔ Enhances credibility

Without 80G registration:

❌ Donors cannot claim tax deduction

❌ Fundraising becomes difficult

12A vs 80G – Key Difference

| Particulars | 12A Registration | 80G Registration |

|---|---|---|

| Benefit To | Trust/NGO | Donor |

| Purpose | Exemption of income | Deduction on donation |

| Section | 12A / 12AB | 80G |

| Mandatory? | Yes, for tax exemption | Optional but highly recommended |

Both registrations serve different but complementary purposes.

Who Can Apply?

The following entities can apply:

✔ Charitable Trust

✔ Public Trust

✔ Society

✔ Section 8 Company

✔ Religious Institution (subject to conditions)

The entity must be registered under applicable laws (Trust Act / Societies Registration Act / Companies Act).

Eligibility Conditions for 12A Registration

To obtain registration under Section 12AB:

1️⃣ The objectives must be charitable as per Section 2(15)

(Relief of poor, education, medical relief, environment protection, etc.)

2️⃣ Activities must be genuine

3️⃣ Income must not be applied for private benefit

4️⃣ Proper books of accounts must be maintained

5️⃣ PAN is mandatory

Eligibility Conditions for 80G Registration

For 80G approval:

✔ Institution must be registered under Section 12A/12AB

✔ It should not benefit any particular religious community or caste (with limited exceptions)

✔ Proper accounts must be maintained

✔ It should not use income for non-charitable purposes

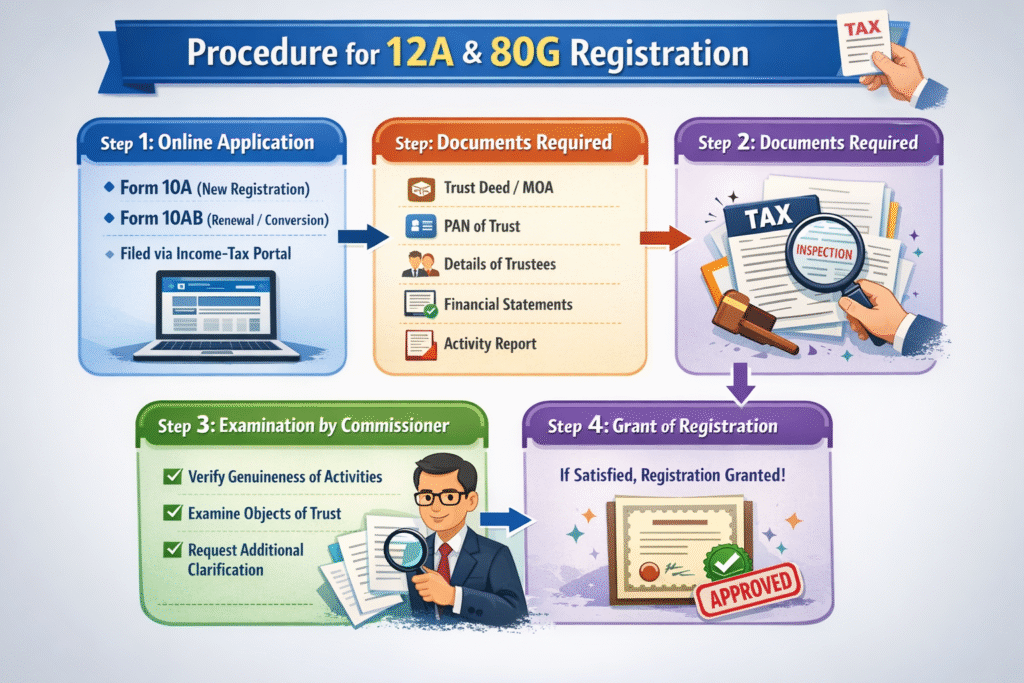

Procedure for 12A & 80G Registration

Step 1: Online Application

Application is filed electronically in:

Form 10A (for new registration)

Form 10AB (for renewal or conversion)

Filed through Income-tax portal.

Step 2: Documents Required

- Trust Deed / MOA / Registration Certificate

- PAN of Trust

- Details of Trustees

- Financial statements (if existing trust)

- Activity report

Step 3: Examination by Commissioner

The Commissioner of Income-tax (Exemptions):

✔ Verifies genuineness of activities

✔ Examines objects of trust

✔ May ask for additional clarification

Step 4: Grant of Registration

If satisfied, registration is granted.

Validity Period

Under the amended provisions:

✔ New registration is generally granted for 5 years

✔ Provisional registration may be granted for 3 years (for new entities)

✔ Renewal application required before expiry

Timely renewal is crucial to avoid cancellation.

Provisional Registration – For New NGOs

If the NGO has not yet started activities:

✔ It can apply for provisional registration

✔ No detailed activity proof required initially

✔ Valid for 3 years

✔ Must apply for regular registration once activities commence

Cancellation of Registration

Registration may be cancelled if:

❌ Activities are not genuine

❌ Income applied for non-charitable purposes

❌ Provisions of law are violated

❌ Return filing is not done

Compliance discipline is very important.

Tax Benefits Under 12A

Once registered:

✔ Income applied for charitable purpose is exempt

✔ 85% application rule applies

✔ 15% accumulation allowed without conditions

✔ Additional accumulation allowed under Section 11(2) (subject to conditions)

Failure to comply may attract taxation.

Deduction Available to Donors Under 80G

Donations may qualify for:

✔ 100% deduction (without limit) – in specific cases

✔ 50% deduction (with or without limit) – general cases

Deduction subject to:

- Mode of payment (cash donation above ₹2,000 not eligible)

- Proper receipt with 80G details

- PAN of trust

- Donation reporting in Form 10BD

Compliance Requirements After Registration

After obtaining registration, trust must:

✔ File Income Tax Return (ITR-7)

✔ Maintain proper books

✔ Get accounts audited (if income exceeds basic exemption limit)

✔ File Statement of Donations (Form 10BD) for 80G

✔ Issue Donation Certificate (Form 10BE)

Non-compliance may result in penalties and cancellation.

Common Mistakes to Avoid

⚠️ Delay in applying for renewal

⚠️ Mixing personal and trust funds

⚠️ Non-maintenance of books

⚠️ Cash donations beyond permitted limits

⚠️ Non-filing of Form 10BD

Professional guidance is advisable.

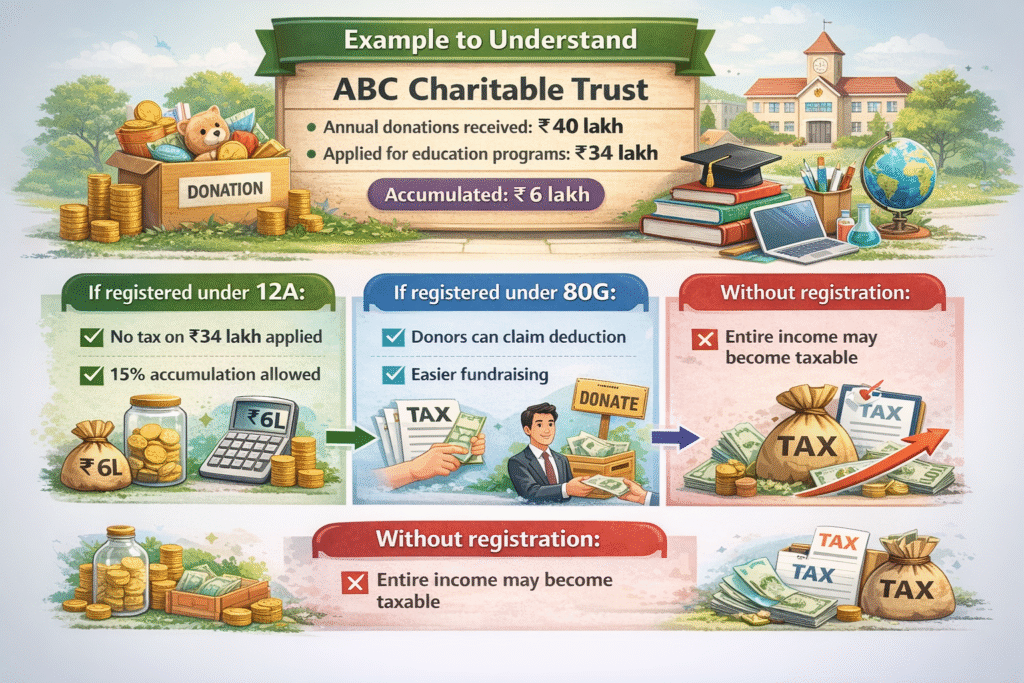

Example to Understand

ABC Charitable Trust:

Annual donations received: ₹40 lakh

Applied for education programs: ₹34 lakh

Accumulated: ₹6 lakh

If registered under 12A:

✔ No tax on ₹34 lakh applied

✔ 15% accumulation allowed

If registered under 80G:

✔ Donors can claim deduction

✔ Easier fundraising

Without registration:

❌ Entire income may become taxable

Why 12A & 80G Matter

Proper registration:

👉 Saves tax

👉 Builds credibility

👉 Attracts donors

👉 Ensures legal compliance

👉 Supports long-term sustainability

NGOs working without registration risk heavy tax exposure.

Quick Decision Table

| Situation | 12A Required? | 80G Required? |

|---|---|---|

| Want income tax exemption | Yes | Optional |

| Want donors to claim deduction | Yes (practically) | Yes |

| New NGO, no activity started | Apply provisional | Can apply |

| Expired registration | Renewal required | Renewal required |

Key Takeaways

✔ 12A registration gives income tax exemption to NGO

✔ 80G gives tax deduction benefit to donors

✔ Registration is now time-bound and requires renewal

✔ Compliance after registration is equally important

✔ Proper documentation ensures smooth approval

Final Thought

Charity begins with intention — but sustainability requires compliance.

12A and 80G registrations are not just legal formalities; they are foundational pillars for a transparent and credible charitable organization.

👉 Apply timely

👉 Maintain proper records

👉 Stay compliant

Smart compliance builds strong institutions.

Is audit mandatory for a trust registered under 12A?

Yes, if the total income (before claiming exemption) exceeds the basic exemption limit, accounts must be audited and audit report filed in Form 10B.

What happens if 12A/80G registration is not renewed on time?

Failure to renew within the prescribed time may lead to lapse of benefits, and income may become taxable until fresh registration is granted.

Are cash donations eligible for 80G deduction?

Cash donations exceeding ₹2,000 are not eligible for deduction under Section 80G. Donations should be made through prescribed banking modes for eligibility.

What is the 85% application rule under 12A?

A registered trust must apply at least 85% of its income for charitable purposes during the year to claim full exemption.

What is Form 10BD and why is it important?

Form 10BD is the annual statement of donations that must be filed by institutions registered under 80G, enabling donors to claim tax deduction.

Leave A Comment