7 Unlocking Amazing Home Loan Tax Benefits for You!

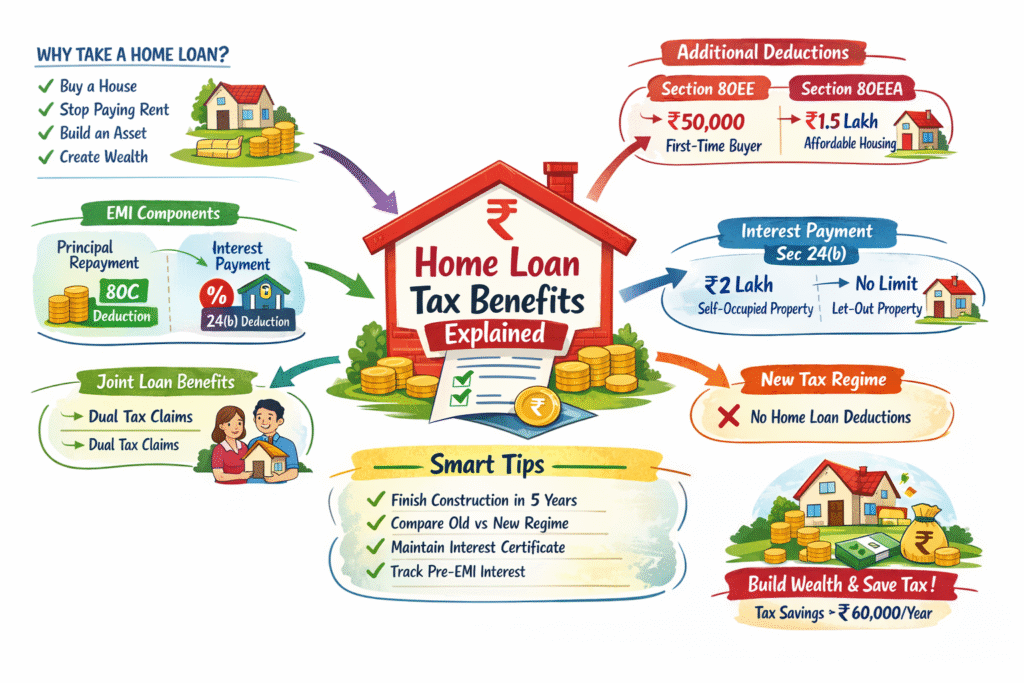

Why do people take a home loan?

To buy a house.

To stop paying rent.

To build an asset.

To create long-term wealth.

But there is another powerful advantage many homeowners overlook:

Tax savings.

A properly structured home loan does not just help you acquire property — it can significantly reduce your income-tax liability under the Income-tax Act, 1961.

Let’s break it down in a simple and structured way.

What Makes a Home Loan Tax-Efficient?

When you repay your home loan, every EMI consists of two components:

✔️ Principal repayment

✔️ Interest payment

Both components are eligible for tax deduction — but under different sections and subject to specific conditions. Understanding how each works can help you maximize your savings.

1️⃣ Deduction on Principal Repayment – Section 80C

The principal portion of your home loan EMI qualifies for deduction under Section 80C.

Maximum Deduction:

₹1.5 lakh per financial year (combined limit under Section 80C)

However, this is not an exclusive limit for home loans. It includes other eligible investments such as:

- Life Insurance premium

- Employee Provident Fund (EPF)

- Public Provident Fund (PPF)

- ELSS investments

- Children’s tuition fees

- And other notified instruments

So, if you are already exhausting your ₹1.5 lakh limit through other investments, the principal repayment may not provide additional benefit.

Important Conditions:

✔️ Deduction is allowed only after construction is completed

✔️ Loan must be taken from a recognized financial institution

✔️ Property should not be sold within 5 years of possession — otherwise deduction claimed earlier may be reversed

Example:

Principal repaid: ₹1,20,000

Other 80C investments: ₹50,000

Total = ₹1,70,000

Eligible deduction = ₹1,50,000 (maximum cap)

2️⃣ Deduction on Interest – Section 24(b)

This is where the major benefit lies.

For Self-Occupied Property:

Maximum deduction allowed = ₹2,00,000 per year

Conditions:

✔️ Loan taken for purchase or construction

✔️ Construction completed within 5 years from end of financial year in which loan was taken

If construction exceeds 5 years, deduction is restricted to ₹30,000 per year.

For Let-Out Property:

✔️ No upper limit on interest deduction

✔️ However, set-off of loss from house property against other income is restricted to ₹2,00,000 per year

✔️ Remaining loss can be carried forward for 8 years

Example:

Interest paid during year: ₹2,60,000

Allowed deduction: ₹2,00,000

Balance ₹60,000 → no immediate benefit (self-occupied case)

For taxpayers in the 30% slab, ₹2 lakh deduction can result in approximately ₹60,000 tax savings (excluding cess).

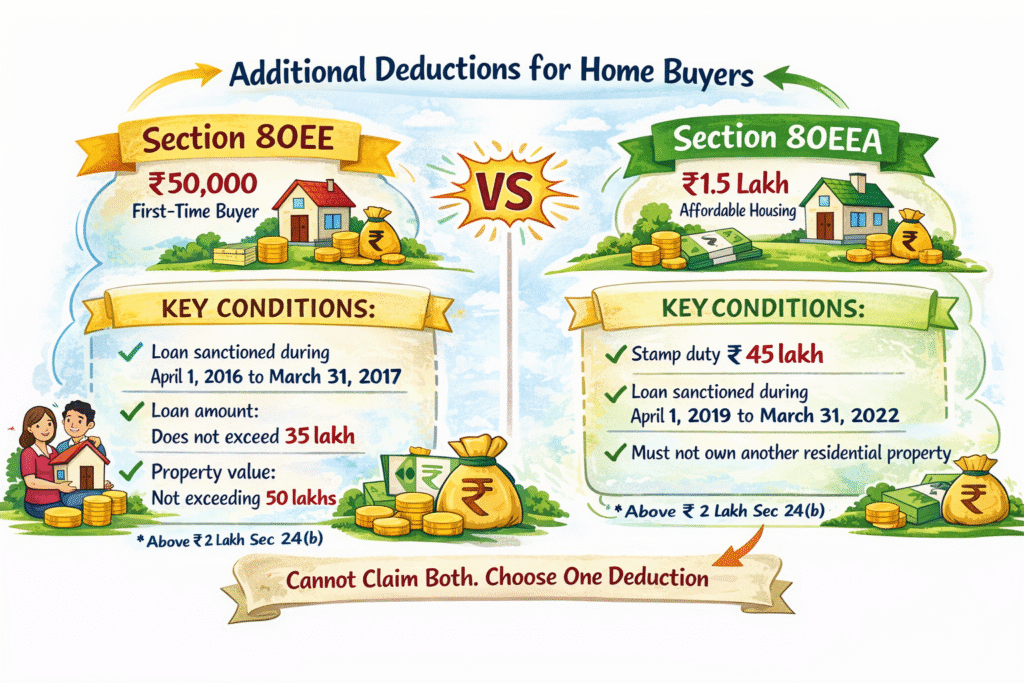

3️⃣ Additional Deduction – Section 80EE

This section provides extra relief to first-time home buyers.

Maximum additional deduction:

₹50,000 per year

This deduction is over and above the ₹2 lakh allowed under Section 24(b).

Key conditions include:

✔️ Loan sanctioned during specified period (April 1, 2016, to March 31, 2017)

✔️ Loan amount within prescribed limit (does not exceed 35 lakh)

✔️ Property value within notified threshold (not exceeding 50 lakhs)

✔️ Individual should not own any other residential property at the time of sanction

4️⃣ Additional Deduction – Section 80EEA

Introduced to promote affordable housing.

Maximum additional deduction:

₹1,50,000

This is also over and above Section 24(b).

Conditions broadly include:

✔️ Stamp duty value within prescribed limit (Stamp Duty is less than or equal to 45 lakh)

✔️ Loan sanctioned within notified period (April 1, 2019, to March 31, 2022)

✔️ Individual should not own any other residential property

Note: Deduction under Section 80EEA cannot be claimed if Section 80EE is claimed.

5️⃣ Pre-Construction Interest Benefit

Interest paid before completion of construction is NOT LOST.

It can be claimed:

✔️ In 5 equal installments

✔️ Starting from the year in which construction is completed

✔️ Subject to overall limit of ₹2 lakh (for self-occupied property)

Many taxpayers miss this important benefit.

ALSO READ : Income Tax Refund 2025 Income Tax Refund in India: Complete Guide to Process, Status & Reissue (2025)

6️⃣ Joint Home Loan – Double Advantage

If the property is jointly owned and both individuals are co-borrowers, each co-owner can claim deductions separately.

Each co-owner can claim:

✔️ Up to ₹2,00,000 for interest under Section 24(b)

✔️ Up to ₹1,50,000 for principal under Section 80C

This significantly increases the total tax benefit for families, provided repayment is made from respective incomes.

7️⃣ Under-Construction Property – Key Rule

Before possession:

❌ Principal deduction is not allowed

❌ Interest deduction is not allowed (except accumulated pre-construction benefit later)

Tax benefits start only after completion or possession certificate is obtained.

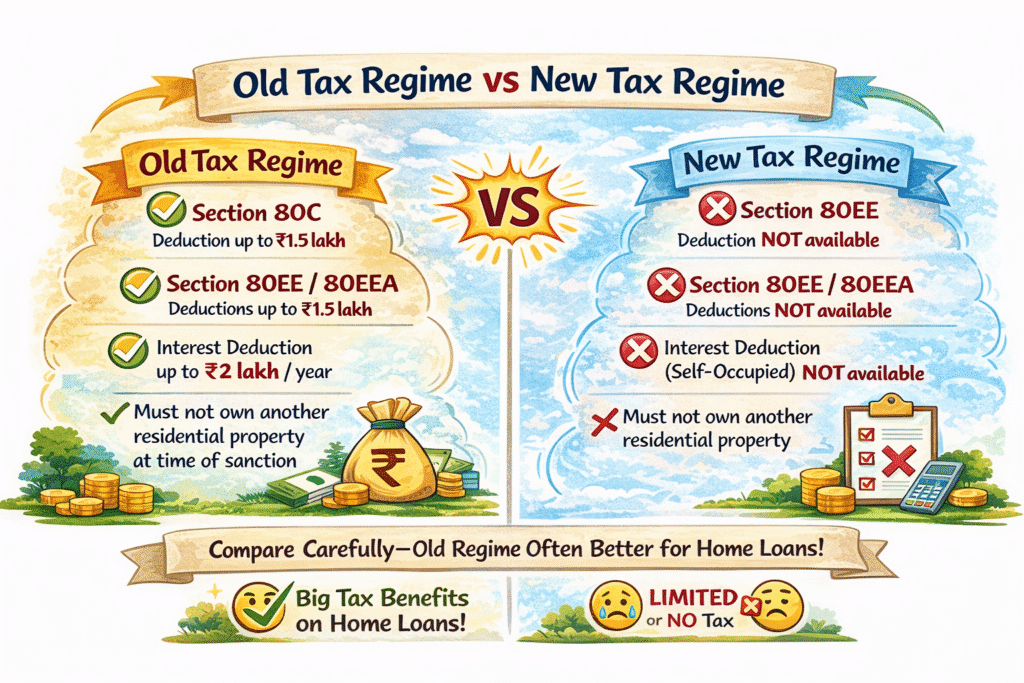

8️⃣ Old Tax Regime vs New Tax Regime

This comparison is crucial.

Under the new tax regime:

❌ Section 80C deduction not available

❌ Section 80EE / 80EEA deductions not available

❌ Interest deduction for self-occupied property not available

Interest deduction may be available only in limited situations for let-out property.

Therefore, home loan tax benefits are primarily effective under the old tax regime. Always compute both options before making your choice.

Quick Summary

| Component | Section | Maximum Deduction |

|---|---|---|

| Principal | 80C | ₹1.5 lakh |

| Interest (Self-Occupied) | 24(b) | ₹2 lakh |

| Additional (First-time buyer) | 80EE | ₹50,000 |

| Additional (Affordable housing) | 80EEA | ₹1.5 lakh |

Smart Tax Planning Tips

✔️ Complete construction within 5 years

✔️ Maintain annual interest certificate from lender

✔️ Structure joint ownership carefully

✔️ Track pre-construction interest

✔️ Compare old vs new regime before filing return

✔️ Ensure loan is from a recognized institution

Why This Matters

If you are in the 30% tax bracket and claim full ₹2 lakh interest deduction:

Tax saving ≈ ₹60,000 per year

Over 15–20 years, this becomes a substantial amount.

A home loan is not merely a liability.

It is also a structured financial tool that can reduce tax burden while helping you build a long-term asset.

Final Thought

Buying a home builds stability.

Repaying a home loan builds ownership.

Understanding tax benefits protects your cash flow.

Because in the end —

It’s not just about owning a house.

It’s about owning it wisely.

Can I claim home loan tax benefits if the property is under construction?

No. Principal and regular interest deductions are allowed only after construction is completed. However, pre-construction interest can be claimed in 5 equal installments after possession.

Can both husband and wife claim tax benefits on a joint home loan?

Yes. If both are co-owners and co-borrowers, each can claim separate deductions for principal (Section 80C) and interest (Section 24(b)) based on their share in repayment.

Is stamp duty and registration eligible for deduction?

Yes. Stamp duty and registration charges are allowed under Section 80C within the ₹1.5 lakh limit, but only in the year they are paid.

Can I claim deduction for a second home loan?

Yes. Interest deduction is available even for a second property. However, set-off of total house property loss against other income is restricted to ₹2 lakh per year.

What happens if I sell the property within 5 years?

If sold within 5 years from possession, deductions claimed earlier under Section 80C for principal repayment will be reversed and added back to your income.

Leave A Comment