Capital Gain Taxation: 7 Essential Insights You Need

We invest in shares and mutual funds for one reason:

To build wealth.

Markets rise. NAVs grow. Portfolios expand.

But one critical question arises when you redeem or sell:

How much tax will you pay on the profit?

Because when you sell shares or mutual funds, the profit is taxable under the head “Capital Gains.”

Understanding the rules can significantly improve what you ultimately retain.

Let’s simplify it.

What Is Capital Gain in Shares & Mutual Funds?

When you sell:

Sale Value

– Cost of Acquisition

– Expenses (like brokerage, STT not deductible)

= Capital Gain

This gain is taxable under the Income-tax Act, 1961.

But the tax depends mainly on:

✔️ Type of asset

✔️ Holding period

✔️ Whether Securities Transaction Tax (STT) is paid

✔️ Type of mutual fund

And this is where many investors get confused.

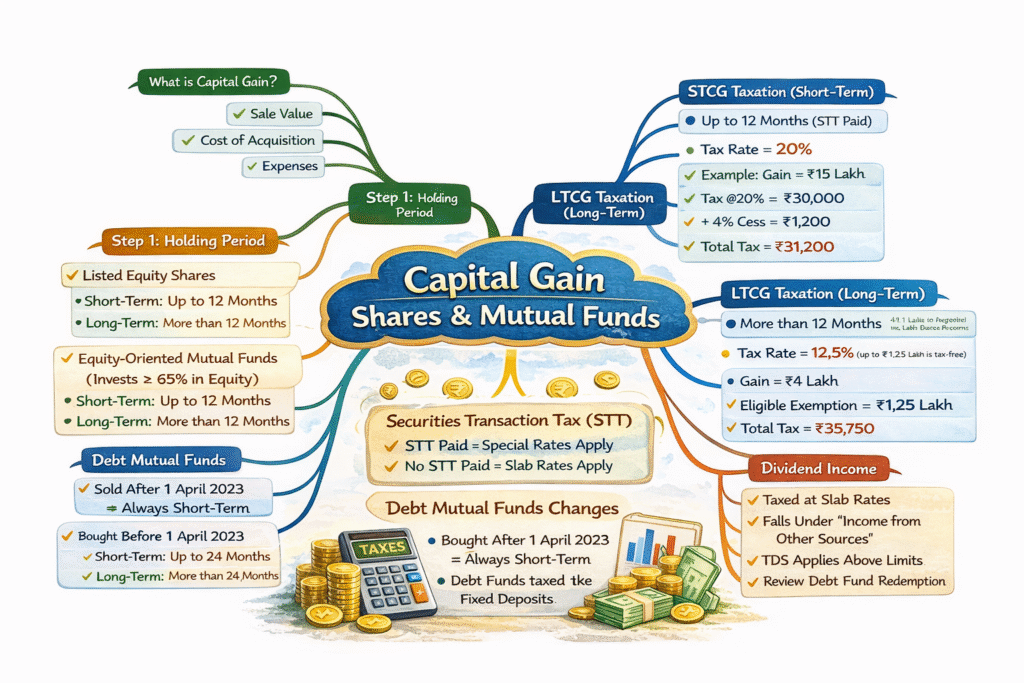

Step 1: Holding Period – The Most Important Factor

1️⃣ Listed Equity Shares (STT Paid)

Held for 12 months or less → Short-Term

Held for more than 12 months → Long-Term

Note: For unlisted equity shares the time limit is 24 months.

2️⃣ Equity-Oriented Mutual Funds

(Schemes investing ≥ 65% in equity)

Held for 12 months or less → Short-Term

Held for more than 12 months → Long-Term

3️⃣ Debt Mutual Funds

The rules depend on date of purchase.

If purchased on or after 1 April 2023:

- Gains are taxed as short-term, regardless of holding period.

- Taxed at normal slab rate

- No indexation benefit

If purchased before 1 April 2023:

- Held up to 24 months → Short-Term

- Held more than 24 months → Long-Term

Long-term gains eligible for 12.5% without indexation or 20% with indexation (subject to conditions under recent amendments).

Short-Term Capital Gain (STCG) – Shares & Equity Funds

If listed equity shares or equity mutual funds are sold within 12 months and STT is paid:

Tax Rate = 20%

(As amended by Finance Act, 2024)

Plus 4% Health & Education Cess

Plus surcharge, if applicable

Example – Short-Term Equity Sale

You bought shares for ₹5 lakh.

You sell them after 8 months for ₹6.5 lakh.

Gain = ₹1.5 lakh

Tax @20% = ₹30,000

Cess @4% = ₹1,200

Total Tax = ₹31,200

Flat rate. No slab benefit.

Long-Term Capital Gain (LTCG) – Shares & Equity Funds

If listed equity shares or equity-oriented mutual funds are held for more than 12 months:

Tax Rate = 12.5%

✔️ Without indexation

✔️ Exemption up to ₹1.25 lakh per year

Only gain exceeding ₹1.25 lakh is taxable.

Plus 4% cess.

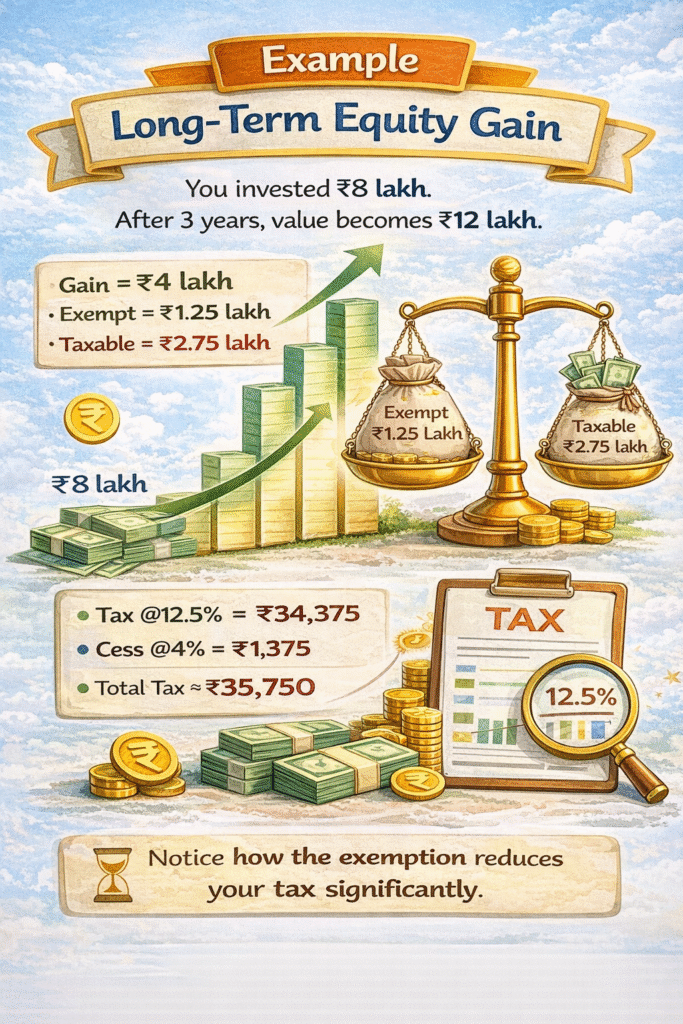

Example – Long-Term Equity Gain

You invested ₹8 lakh.

After 3 years, value becomes ₹12 lakh.

Gain = ₹4 lakh

Exempt = ₹1.25 lakh

Taxable = ₹2.75 lakh

Tax @12.5% = ₹34,375

Cess @4% = ₹1,375

Total Tax ≈ ₹35,750

Notice how the exemption reduces your tax significantly.

What About Securities Transaction Tax (STT)?

For special rates to apply:

✔️ Securities Transaction Tax (STT) must be paid

✔️ Sale must be through recognized stock exchange

Otherwise, normal capital gain provisions may apply.

Debt Mutual Funds – The Big Change

This is where many investors get surprised.

For Units Purchased After 1 April 2023:

Regardless of holding period:

✔️ Taxed at slab rate

✔️ No long-term benefit

✔️ No indexation

So if you are in 30% slab → Gain taxed at 30%

This makes debt funds similar to fixed deposits from a tax perspective.

Indexation – When Available

For eligible long-term non-equity units (acquired before cut-off dates), taxpayers may opt:

✔️ 12.5% without indexation

OR

✔️ 20% with indexation (subject to transitional provisions)

Indexation adjusts cost for inflation and may significantly reduce taxable gain.

Always compute both options.

Capital Loss Rules

Very important for portfolio management.

Short-Term Capital Loss

Can be set off against:

✔️ Short-term gains

✔️ Long-term gains

Long-Term Capital Loss

Can be set off only against:

✔️ Long-term gains

Unadjusted loss can be carried forward for 8 years.

But only if return is filed within due date.

Dividend Income – Separate Treatment

Dividends from shares and mutual funds:

✔️ Taxed under “Income from Other Sources”

✔️ Taxed at slab rate

✔️ TDS applicable above prescribed limits

No longer tax-free in investor’s hands.

Special Situations Investors Miss

❌ Switching between mutual fund schemes – treated as sale

❌ STP transfers – each transfer is taxable

❌ Bonus shares – cost allocation matters

❌ Rights shares – separate cost computation

❌ ESOP sales – separate tax considerations

Every transaction matters.

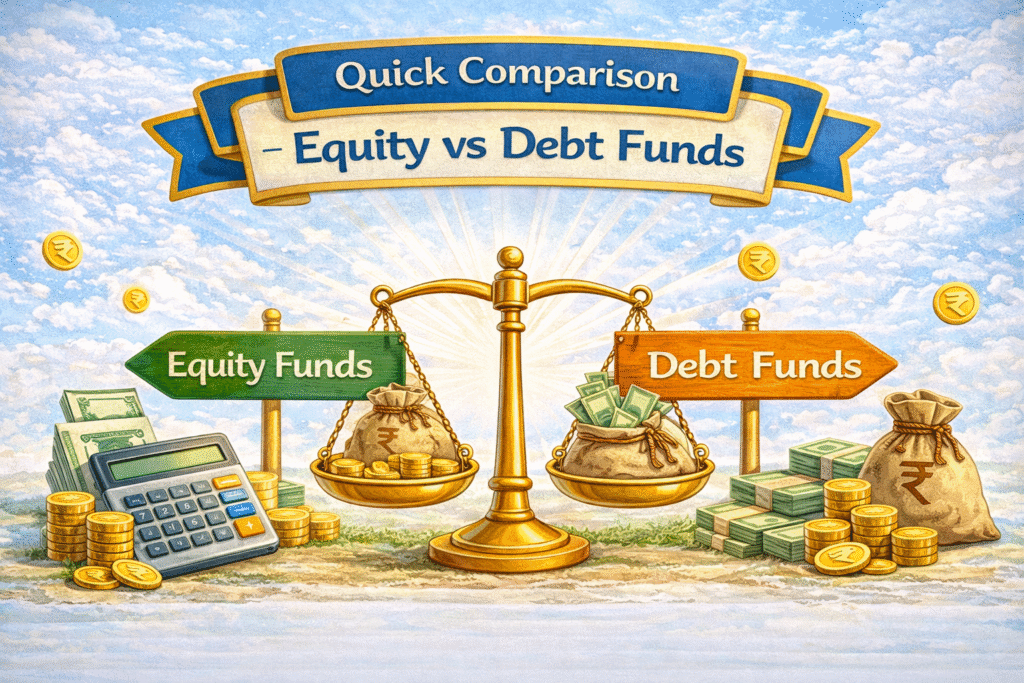

Quick Comparison – Equity vs Debt Funds

| Basis | Equity Shares / Equity MF | Debt Mutual Funds (Post 1 April 2023) |

|---|---|---|

| Short-Term Period | 12 months | Always STCG |

| LTCG Rate | 12.5% | Not available |

| Exemption | ₹1.25 lakh | Not available |

| Slab Taxation | No | Yes |

| Indexation | No | No |

Smart Tax Planning Tips

✔️ Hold equity investments beyond 12 months

✔️ Use ₹1.25 lakh LTCG exemption every year (tax harvesting)

✔️ Harvest losses to offset gains

✔️ Track purchase dates carefully

✔️ Review debt fund purchase date before redemption

✔️ File returns on time to preserve losses

Tax planning is not timing the market.

It is timing your exit wisely.

Why This Matters

Imagine selling shares at 11 months vs 13 months.

That small difference:

Could reduce your tax rate

Could give you exemption benefit

Could save lakhs

Capital gain taxation is not complicated.

It is about:

✔️ Holding period

✔️ Type of asset

✔️ Applicable rate

✔️ Available exemption

When you plan your exit as carefully as your entry,

you maximize wealth retention.

Final Thought

Investing grows your money.

Tax awareness protects it.

Because at the end of the day —

It’s not just what your portfolio earns.

It’s what you keep after tax.

ALSO READ: CIT (LTU) v. Reliance Industries Ltd (2024)

Do I have to pay tax if I reinvest the money in another mutual fund?

Yes. Switching or reinvesting is treated as a sale for tax purposes. Capital gains tax applies even if the amount is immediately reinvested.

Is the ₹1.25 lakh LTCG exemption automatic?

Yes, for eligible listed equity shares and equity mutual funds held over 12 months. Only gains exceeding ₹1.25 lakh in a financial year are taxable at 12.5%.

Can capital losses reduce my overall tax liability?

Yes. Short-term losses can be set off against both STCG and LTCG, while long-term losses can be set off only against LTCG. Unused losses can be carried forward for 8 years.

Are dividends from shares and mutual funds tax-free?

No. Dividends are taxable under “Income from Other Sources” at your slab rate, and TDS may apply above prescribed limits.

Leave A Comment