8 Insane Insights on Capital Gain Taxation You Need to Know

We all invest with one goal in mind — to grow our wealth.

Whether it’s buying property, investing in gold, putting money into debt mutual funds, or purchasing bonds, we expect returns. But here’s something equally important:

What happens when you sell those investments?

The profit you earn is called Capital Gain, and yes — it is taxable.

Understanding how capital gains are taxed (especially for assets other than shares) can make a huge difference in how much money you ultimately keep.

Let’s break it down in simple terms.

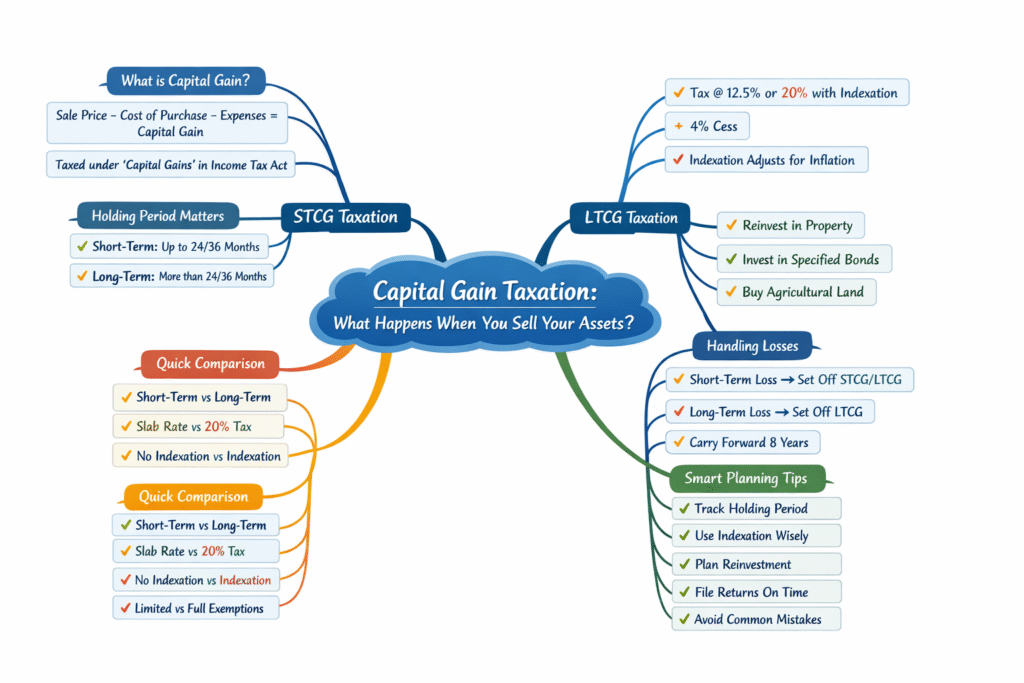

What Exactly is Capital Gain?

When you sell a capital asset, your gain is calculated like this:

Sale Price

– Cost of Purchase

– Expenses related to sale

= Capital Gain

This income is taxed under the head “Capital Gains” in the Income-tax Act, 1961.

But here’s the key part:

The tax you pay depends mainly on how long you held the asset.

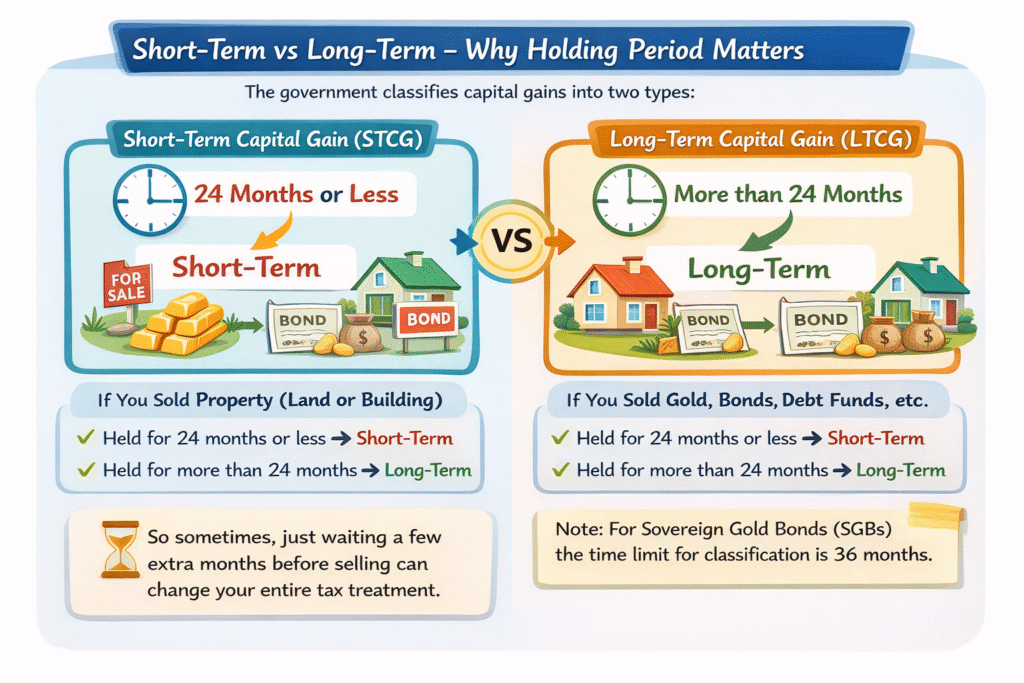

Short-Term vs Long-Term – Why Holding Period Matters

The government classifies capital gains into two types:

- Short-Term Capital Gain (STCG)

- Long-Term Capital Gain (LTCG)

And the difference?

It’s all about time.

If You Sold Property (Land or Building)

- Held for 24 months or less → Short-Term

- Held for more than 24 months → Long-Term

If You Sold Gold, Bonds, Debt Funds, etc.

- Held for 24 months or less → Short-Term

- Held for more than 24 months → Long-Term

Note: For Sovereign Gold Bonds (SGBs) the time limit for classification is 36 months.

So sometimes, just waiting a few extra months before selling can change your entire tax treatment.

Short-Term Capital Gain (STCG) – How It Is Taxed

If you sell an asset within the short-term period:

The gain is added to your total income.

It gets taxed at your normal slab rate.

That means:

- If you are in the 30% slab → You may pay 30% tax

- If you are in the 5% slab → You may pay 5% tax

There is no special rate benefit here.

Example

You bought gold for ₹10 lakh.

You sell it after 2 years for ₹13 lakh.

Since gold requires 24 months to qualify as long-term, this is a short-term gain.

Gain = ₹3 lakh

Tax = As per your income slab

Simple — but sometimes costly if you are in a higher slab.

Long-Term Capital Gain (LTCG) – The Advantage of Patience

If you hold the asset beyond the required period:

You get long-term capital gain treatment.

For most assets other than shares:

- Tax Rate = 12.5% without indexation, or an option for 20% with indexation for properties/assets acquired before July 23, 2024.

- Plus 4% Health & Education Cess

What is Indexation? (The Hidden Tax Saver)

Inflation increases prices over time. The law recognizes this.

Indexation adjusts your purchase cost to account for inflation.

So instead of paying tax on the entire profit, you pay tax only on the inflation-adjusted gain.

This can significantly reduce your tax liability.

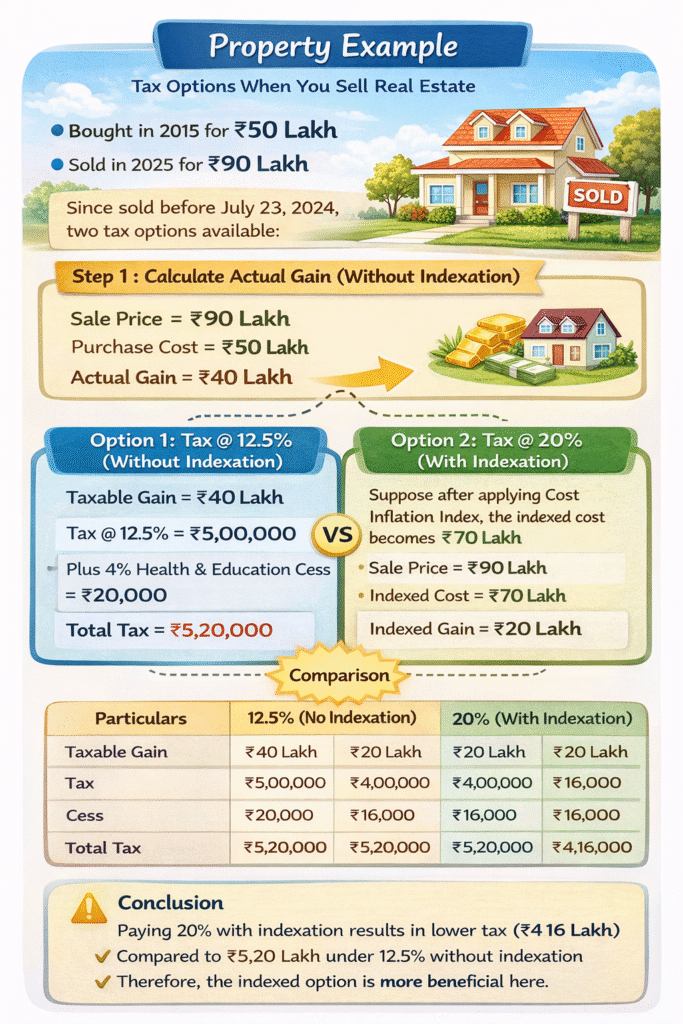

Property Example

You bought a property in 2015 for ₹50 lakh.

You sell it in 2025 for ₹90 lakh.

Since the property was acquired before July 23, 2024, you have two tax options available.

Step 1: Calculate Actual Gain (Without Indexation)

Sale Price = ₹90 lakh

Purchase Cost = ₹50 lakh

Actual Gain = ₹40 lakh

🔹 Option 1: Tax @ 12.5% (Without Indexation)

Taxable Gain = ₹40 lakh

Tax @12.5% = ₹5,00,000

Plus 4% Health & Education Cess = ₹20,000

Total Tax = ₹5,20,000

🔹 Option 2: Tax @ 20% (With Indexation)

Suppose after applying Cost Inflation Index, the indexed cost becomes ₹70 lakh.

Sale Price = ₹90 lakh

Indexed Cost = ₹70 lakh

Indexed Gain = ₹20 lakh

Tax @20% = ₹4,00,000

Plus 4% Cess = ₹16,000

Total Tax = ₹4,16,000

Comparison

| Particulars | 12.5% (No Indexation) | 20% (With Indexation) |

|---|---|---|

| Taxable Gain | ₹40 lakh | ₹20 lakh |

| Tax | ₹5,00,000 | ₹4,00,000 |

| Cess | ₹20,000 | ₹16,000 |

| Total Tax | ₹5,20,000 | ₹4,16,000 |

Conclusion

In this case:

- Paying 20% with indexation results in lower tax (₹4.16 lakh)

- Compared to ₹5.20 lakh under 12.5% without indexation

Therefore, the indexed option is more beneficial here.

However, this may vary depending on:

- Year of purchase

- Inflation impact

- Holding period

So, taxpayers should compute both options before finalizing tax liability.

Important Update – Debt Mutual Funds

Recent amendments have changed taxation for certain debt mutual funds purchased after a specified date.

In some cases:

- Indexation benefit may not be available

- Gains may be taxed at slab rates

So always check:

- Type of fund

- Date of purchase

- Applicable rules

Details matter here.

What If You Have Losses?

Losses are not always bad — at least in tax terms.

Here’s how adjustments work:

- Short-Term Capital Loss → Can be set off against both short-term and long-term gains

- Long-Term Capital Loss → Can be set off only against long-term gains

Unused losses can be carried forward for 8 years, but only if you file your return on time.

So timely filing is crucial.

Can You Save Tax on Long-Term Gains?

Yes, especially for property.

You may claim exemption if you:

- Reinvest in another residential house

- Invest in specified bonds

- Reinvest in agricultural land (subject to conditions)

With proper planning, tax on property sale can be reduced or even fully eliminated.

Short-Term vs Long-Term – Quick Comparison

| Basis | Short-Term | Long-Term |

|---|---|---|

| Holding Period | Up to 24/36 months | More than 24/36 months |

| Tax Rate | Slab rate | 20% |

| Indexation | No | Yes |

| Exemptions | Limited | Available |

Why This Matters So Much

Let’s say you plan to sell property after 23 months.

If you wait 2 more months, it becomes long-term.

That small delay could:

- Lower your tax rate

- Give you indexation

- Open up exemption options

Sometimes, timing alone changes everything.

Capital gain taxation is not just about compliance —

It is about making smarter financial decisions.

Smart Planning Tips

✔️ Track your purchase date carefully

✔️ Hold property beyond 24 months where possible

✔️ Use indexation wisely

✔️ Plan reinvestment in advance

✔️ File returns on time to preserve losses

Tax planning is not about avoiding tax.

It’s about understanding the rules and using them correctly.

Common Mistakes People Make

❌ Selling just before long-term threshold

❌ Ignoring indexation benefit

❌ Not claiming transfer expenses

❌ Missing exemption timelines

❌ Forgetting to file return in loss year

A little awareness can prevent costly errors.

Final Thought

Investing is important.

But retaining your returns after tax is even more important.

Capital gain taxation is not complicated once you understand:

- Holding period

- Applicable rate

- Indexation

- Exemptions

When you plan your exit as carefully as your investment,

you protect your wealth.

Because at the end of the day —

It’s not just what you earn.

It’s what you keep.

ALSO READ: Capital Gain Taxation: 7 Essential Insights You Need

Is indexation always beneficial for long-term capital gains?

Not always — you should calculate both 12.5% without indexation and 20% with indexation (where available) to see which results in lower tax.

Can I reduce tax on property sale legally?

Yes, by reinvesting in a residential house, specified bonds, or eligible assets within prescribed timelines, subject to conditions.

Can capital losses help reduce my tax liability?

Yes, short-term losses can offset both STCG and LTCG, while long-term losses can offset only LTCG and can be carried forward for 8 years if return is filed on time.

Leave A Comment